Good day traders! Check now the most recent charts and market updates for today’s session. Learn more about analysis and be updated on the current happenings in the market!

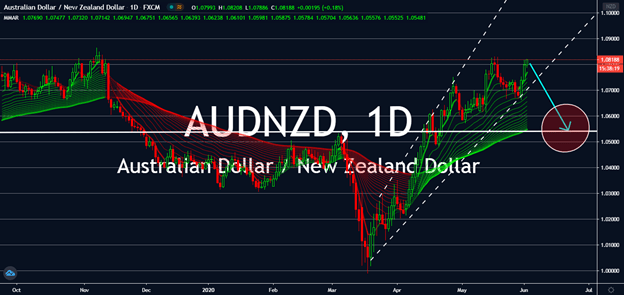

AUDNZD

The Reserve Bank of Australia retained its interest rates at 0.25% today following its outperformance against several other currencies yesterday. It looks like if they’d changed the figure, it might not have changed anything amid increasing US/China tensions, general negativity over macroeconomic data sets, and violent protests in the US. Commodity and risk-sensitive countries like Australia have been rising since, especially after the Aussie dollar reached 3-month highs for several exchanges. However, markets think the recent rallies are in preparation for an upcoming sell-off as the conflict between the US and China continues through the months. Meanwhile, the broader market is fixated on the broader risk of how worldwide events will turn out for each countries’ economies. If equities and risk demand rise, the AUD might see a prompt recovery despite trade tensions and speculations.

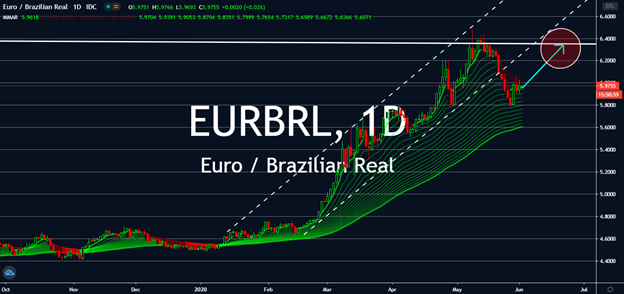

EURBRL

It looks like both the Euro and the Brazilian real aren’t seeing good trajectories this week as both economies show negative news and figures. Brazil’s national economy shrank 1.5% in the first three months this year, which was down from a revised 0.4% jump during the previous quarter in 2019. The drop was the first contraction since 2016, as well as the biggest decline since early 2015. Several sectors like finance, mining, manufacturing, construction, and public administration all met significant slumps throughout the period. Although the HIS Markit manufacturing purchasing managers index saw a higher-than-estimated figure on Monday, which came in at 38.3 in May against April’s 36 low. Meanwhile, conflicts with Britain continues to affect the already failing economy in Europe. Nonetheless, Brazil’s new status as a coronavirus epicenter is expected to push its economy down against the single currency.

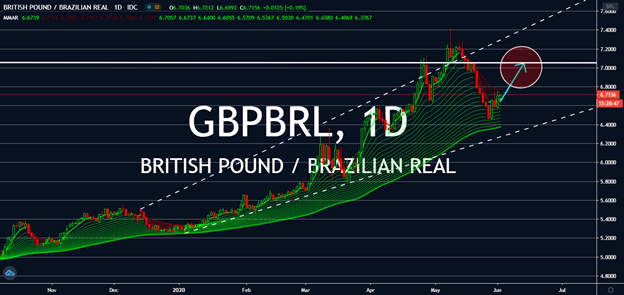

GBPBRL

The British pound saw solid gains against its closest rivals yesterday with GBP seeing better manufacturing results than Germany—the UK Final May manufacturing PMI came in a 40.7 against a previous estimate that sat around 40.6. Germany’s respective figure came in at 36.6, which was not only lower than the UK but also lower than market estimates. On that note, Brazil’s recent report of a lower quarterly economy in comparison to the last quarter of 2019 is set to push its currency down against sterling pound as long as the UK continues to see positive figures in the coming months. In fact, its GDP shrank 1.5% during that period, the first contraction since 2016, down against the revised 0.4% achieved the previous quarter. The UK also passed its crown as the coronavirus epicenter to Brazil, which could in many ways push the currency down against a number of rivals, especially the sterling pound.

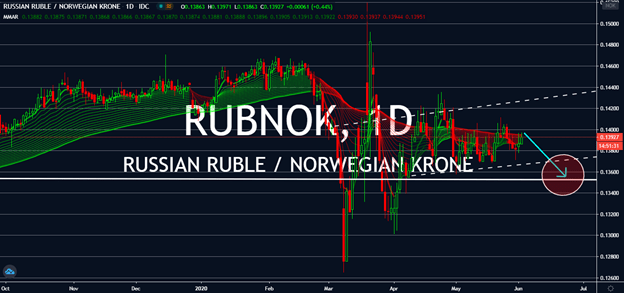

RUBNOK

The Russian ruble saw its pre-coronavirus levels on Monday thanks to better oil progress since the beginning of March. This was led by the Russian government’s decision to delink the currency from its oil prices earlier this year, which was an aftermath of the 2014 to 2015 economic crisis in the country. Moreover, investors have been paying close attention to what could happen between the latest OPEC+ deal between Russia, Saudi Arabia, and other major oil producers. The organization reduced the daily global supply of oil to a record low by 10% through its production cut agreement in May and June, but it will wind down by the end of this month. The lack of a new deal in the organization signals a higher demand for the commodity, which could help oil-dependent countries in the long run. Although the ruble could win against the krone in short-term, Goldman Sachs expects the oil-sensitive Norwegian krone to rise in the coming months, instead.